Meet our CODE_n CONTEST Finalists 2016: Ginmon from Germany

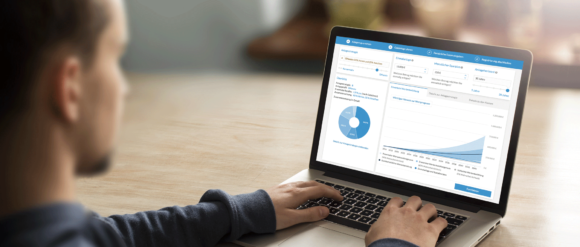

![]() CODE_n CONTEST Finalist Ginmon allows customers to invest money in a globally diversified portfolio based on proven scientific methods. Customers gain access to high returns while enjoying the low risk associated with broad investments in over 10,000 companies in 47 countries. The FinTech startup provides a transparent, all-inclusive solution that enables customers to understand their investments and give them the feeling their finances are in safe hands. How? That’s what CEO and founder Lars Reiner, told us in this interview.

CODE_n CONTEST Finalist Ginmon allows customers to invest money in a globally diversified portfolio based on proven scientific methods. Customers gain access to high returns while enjoying the low risk associated with broad investments in over 10,000 companies in 47 countries. The FinTech startup provides a transparent, all-inclusive solution that enables customers to understand their investments and give them the feeling their finances are in safe hands. How? That’s what CEO and founder Lars Reiner, told us in this interview.

What is Ginmon all about? How did you come up with the idea?

Lars:Ginmon is all about providing a modern and efficient personal wealth management. While working for one of biggest commercial banks in Germany I realized that proven scientific concepts were often not offered to customers. Those concepts are taught around the globe and proven many times. Banks do not offer products based on those concepts because they are very low margin and not as profitable as traditional products. Therefore to really profit from professional wealth management one has to study investment theory and do it himself or pay horrendous sums to personal wealth managers. Additionally it seemed to me that large companies could not or did not want to react and adapt to the possibilities digitalization provided. As a technology and innovation loving person I had a concrete idea about how customers could benefit from digitalization, but the established financial industry did not provide me with the right setting to implement those ideas. Finally the request of many friends and family members who were looking for a solution to build wealth efficiently triggered my decision to start Ginmon. To put it in a nutshell: I wanted to implement the ideas I had for digital wealth management, provide an investment concept which was up date only restricted to professionals and last but not least enable my friends and family members to build up wealth efficiently.

“Digital Disruption“ – that’s the motto of this year’s CODE_n CONTEST. What makes your solution innovative, what makes it disruptive?

Lars: The innovation behind Ginmon is the combination of scientific wealth management concepts and technology which allows us to automate and improve essential processes. Especially constant rebalancing and anticyclical investment, which is significantly improved using our algorithm, enables us to optimize the risk/return profile of our customers. We can offer a better product at lower costs and thereby compete with the established industry and disrupt existent structures.

Additionally, we focus on customer needs that were not answered before. We believe that besides profit, customers want to keep control over their investments, stay flexible and really understand what their money is doing respectively the strategy behind it, as well as being supported in a professional and personal manner. The biggest part of our customers have a lot of capital market experience themselves but understand the benefits of a solution which allows them to be invested optimal at any time without any effort.

You’re one of the 13 finalists in the Applied FinTech contest cluster. Which challenges do you think young companies have to face in this sector? How do you handle these challenges?

Lars: The culture in Germany seems to be very conservative when it comes to financial products.Therefore new concepts sometimes do not accelerate as fast as in other countries. But when a product is accepted Germany is a very valuable market.

A possibility to handle this are cooperations with existing and known companies. Here FinTechs can profit from known brands and established companies can profit from innovative business models and concepts.

What does Robo Advisory do better than the classical bank advisor?

Lars: First of all classical bank advisors still do not advise in many cases but sell products they earn the highest margins on, e.g. provision based products, or products compiled by the bank they work for. In fact they actually have to sell these products to make their service profitable. It is very cost intensive to provide in person advisory, because of costs for leases, regulatory requirements and headcount required. Because we can automate essential processes we are able to drive down costs and therefore choose products only because of their quality.

Secondly, our investment strategy gets implemented by an unemotional algorithm and is therefore able to follow strategies which are hard to follow by human investors. For example our constant rebalancing and anticyclical investment by which we optimize the risk/return rate.

Last but not least, transparent and easy-to-use solutions fit the needs of our customers much better than in person advisory with appointments at times when you should actually be working and have no possibilities to compare products or inform yourself during decision making. Our customers decide and inform themselves online, they don’t want to get something sold but understand the quality of the solution and then buy based on an informed and rational decision.

Thanks for the interview, Lars!

Write a comment